The mounting cost of higher education and advanced training remains a pivotal cause of concern in America. Reportedly, the average tuition fees have risen outrageously in the last 20 years, with an inflation rate of 4.70% each year. According to BLS (Bureau of Labor Statistics), education prices were 245.47% higher in 2020 than in 1993. It has surpassed the average hourly wages & housing prices, which triggers unaffordability. Due to the ever-increasing tuition fees, there has also been a surge in student debt, reaching $1.7 trillion in 2021.

Fortunately, there exists an alternative to traditional student loans that can help you procure advanced training with no cost commitment. ISA or Income Share Agreement brings new hope for students to pursue a risk-free education. Let’s examine the benefits of using ISA to get higher education & training.

A Synopsis of the Income Share Agreement

ISA or Income Share Agreement is a contract between the school & the student. Under the Income Share Agreement, the school agrees to fund students’ educational expenses in exchange for a fixed percentage of their post-graduate earnings for a set period.

ISA is an effective way to pay for advanced training & education by sharing a percentage of your future income instead of burdening yourself with monthly student loan installments. We will discuss innumerable benefits of using ISA over student loans later in the blog.

What is the need for an Income Share Agreement?

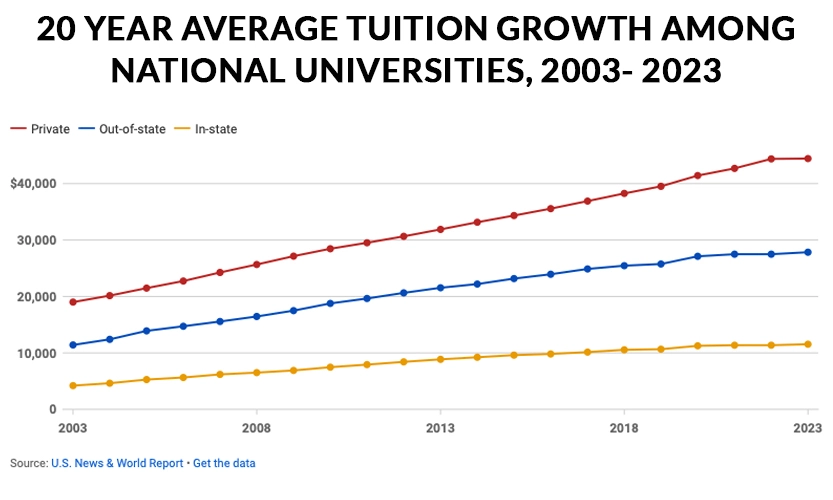

The inflation in the cost of higher education is a matter of concern. If we do a quick statistical breakdown of the increased average tuition fees at a Private National University, Out-of-State & In-State Public National Universities, we’ll get some staggering results as given below:

- The average tuition fees at Private National Universities have jumped by 144%.

- The tuition fees of an Out-of-State Public National University have also hiked by 165%.

- While the In-state Public National University’s tuition fees have grown the most by a whopping 212%.

It has been predicted that by 2033 the tuition fees in Public & Private National Universities will be as high as $94,800 & $323,900 per annum.

Considering the amount of undue pressure on students to pay such escalating fees, adopting the Income Share Agreement on a massive scale has become indispensable. ISA facilitates risk-free education, wherein the students are not liable to pay anything till they graduate and start earning. For instance, if a student loses his job or doesn’t get the highest-paying job to meet the minimum threshold of ISA, his payments automatically get waived until he restores financial stability.

Benefits of ISA over the Traditional Student Loan

If you’re wondering which one is better amongst ISA vs Student Loans, let’s compare them on some common factors to understand the benefits of using ISA over student loans:

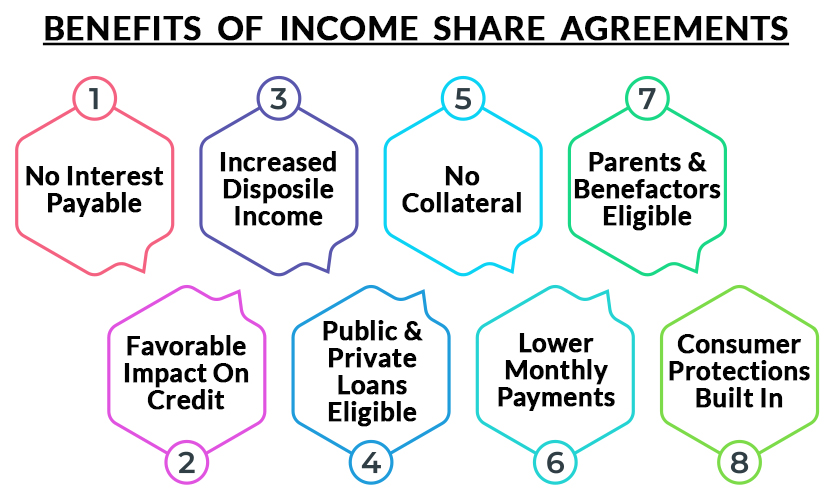

Greater Flexibility to Pay:

ISA provides greater flexibility to students to make repayments. The students only need to reimburse a fixed percentage of their income once employed. Also, payments are deferred if the students are not earning a minimum salary threshold. In contrast, Student loans don’t provide much flexibility in making repayments. It compels students to repay their loan installments each month with the added interest regardless of their unemployment & poor financial status. Thus, ISA is more beneficial than student loans in terms of flexibility.

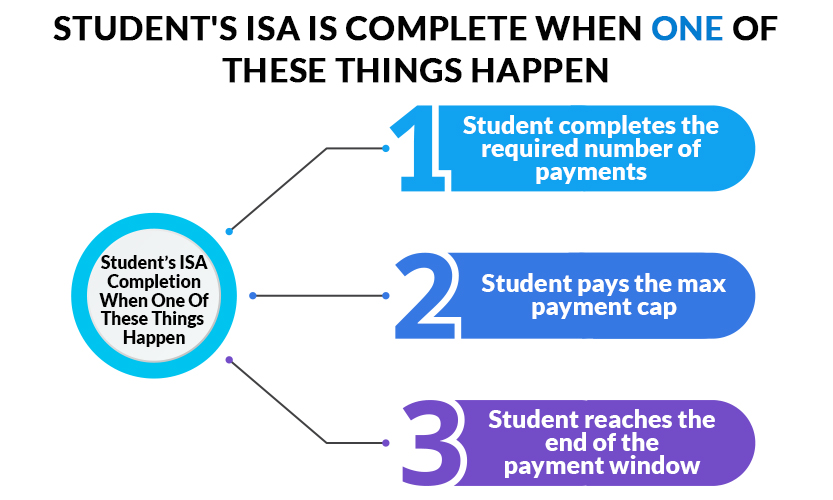

Set Duration for Making Payments:

The maximum payment window of an Income Share Agreement ranges between 2 to 10 years. Hence, if a student fails to make all the monthly repayments by the end of the payment window, his payment obligation automatically gets terminated. However, there is no maximum payment window in student loans that bound students for years until they pay off the student loan amount.

Secures Students from Paying Excessively:

There is a payment cap or the maximum payment that the student agrees to pay under the Income Share Agreement. It protects students with higher incomes from making unreasonably high payments to the school. Also, their ISA obligation ends once the students pay the maximum payment cap. The payment cap could be 1.0x or 2.5x the student loan amount. On the other hand, student loans often have a higher interest rate, leading to a hefty debt for the student.

Provides a Career Surety:

With an ISA, schools reaffirm to students that their advanced training can help them acquire the skills to land a job in their desired field or gain a suitable position. Thus, ISA adds to the school’s credibility and shows its willingness to share the risks & rewards with the students. So, one should always look for Bootcamps with a higher income threshold, which not only empowers candidates to secure a high-paying job but also gives them the flexibility to make no monthly payments until their gross income is less than the set amount. In contrast, student loans do not guarantee any career success for students, which is why many students remain unemployed with loads of debt.

Payments Start when Income Starts, Which is a Win-Win:

It is one of the significant benefits of using an ISA. ISA has a minimum threshold which refers to the minimum annual income students must make before making repayments. ISA does not enforce any financial burden on the students unless their annual income meets the minimum threshold. For instance, if the minimum threshold of an ISA is $40,000, a student is free from any repayment obligation if his annual income is less than this amount. However, this isn’t the case with student loans, as students need to start making monthly loan payments while pursuing their courses. If the students cannot make payments due to financial hardships or any other issue for 270 days, their student loan officially goes into delinquency or default status. Even if Students don’t get jobs, they still have to pay their student loans which is not the case with an ISA.

Many universities, colleges, and Bootcamps facilitate ISAs to increase the accessibility of advanced training and education for students. ISA can fill the funding gaps for students by shifting the financial risk from students to schools

ISA is a robust funding model that can replace student loans in the coming years. An ISA or Income Share Agreement is not a loan since there is no principal balance, accruing interest, or penalty for making fewer payments than the funded amount. Besides, the money advanced in ISA is an investment in the students’ future earning potential.

ISA differs from School to School

Many Bootcamps & Universities follow different criteria for Income Share Agreements, including payment terms, minimum threshold, and income share percentage.

Some Bootcamps have a minimum threshold of $40,000, meaning that if a candidate secures a job at a salary as low as $40,000 per annum, he will be liable to make monthly payments.

We at SynergisticIT have kept a minimum threshold of $81,000, so if the annual salary of our candidate is less than $81,000, we don’t hold any monthly payments; rather, the payments are waived for that period. Only once a candidate makes over $65,000 or higher the ISA payment starts.

Another thing that one needs to check is the income share percentage offered by Bootcamp. Several Bootcamps take as much as 15% to 18% of the student’s post-graduate salary with a payment cap of 2.5x. Thus, the students pay far more than the amount borrowed with their increased annualized salaries. Therefore, it is essential to comprehend the terms of ISA before enrolling in any Bootcamp or University for advanced training. Let’s take an example to get a better understanding of ISA. For instance, if your student loan amount is $25000, the maximum payment cap is $30,000 & you need to pay 12% of your income for 4 years with the minimum income threshold of $65,000. Here is what you need to pay as per different income levels.

| Annual Income | Monthly Payment | Total Payment in 1st year | Total Payment in 2nd year | Total Payment in 3rd Year | Total Payment in 4th Year |

| $64,000 | $0 | $0 | $0 | $0 | $0 |

| $68000 | $680 | $8160 | $8160 | $8160 | $5,520 |

| $72,250 | $723 | $8,670 | $8,670 | $8,670 | $3,990 |

| $76,500 | $765 | $9,180 | $9,180 | $9,180 | $2,460 |

| $80,750 | $808 | $9,690 | $9,690 | $9,690 | $930 |

| $85,000 | $850 | $10,200 | $10,200 | $9,600 | $0 |

| $93,500 | $935 | $11,220 | $11,220 | $7,560 | $0 |

| $97,750 | $977 | $11,730 | $11,730 | $6,540 | $0 |

| $102,000 | $1,020 | $12,240 | $12,240 | $5,520 | $0 |

| $106,250 | $1,063 | $12,750 | $12,750 | $4,500 | $0 |

Under Income Share Agreement, you must pay a fixed percentage of your monthly salary for up to a maximum payment cap. Unless your annual income meets the minimum threshold of $65000, you don’t need to pay anything. The above table compares monthly & total ISA payments for different income levels.

Early Termination or Cancellation of ISA

All Bootcamps allow students to cancel their Income Share Agreement based on different terms & conditions. Have a look at the procedure for cancelation or early termination of ISA:

- Students can cancel an ISA within a certain number of days from its effective date. If you cancel your agreement during that time, no cost will be imposed on you & you will be withdrawn from the program without further obligations.

- If you withdraw or abandon your program after the specified Cancellation Period, you may be responsible for paying a portion or all of your ISA amount up to the payment cap. Students must refer to their respective agreements for complete details.

- Students may also terminate their ISA early at any time by paying the Payment Cap in effect for such period, less all previously paid Monthly Payments in addition to any outstanding fees owed (if any). You may also be eligible for an incremental payment cap as depicted below as an example:

| Contract Term (Months) | Incremental Payment Cap |

| 1 to 12 | $25,000 |

| 13 to 24 | $27,000 |

| 25 to 36 | $28,000 |

| 37+ | $30,000 |

Conclusion

There are unlimited options for students looking to upskill with online training; however, finding quality courses that can translate to higher earnings is difficult. An Income Share Agreement or ISA can be a game-changing funding model to pay tuition fees. Instead of overburdening the students with decades of debt, it offers a short-term solution that ensures students’ success.

We at SynergisticIT provide the option of Income Share Agreement for each of our technology upskill programs, including Java, AWS, MERN Stack, Machine Learning, Data Science, & Python. Our terms of the Income Share Agreement are flexible as we want our candidates to grow in their careers & procure higher-paying jobs.

Connect with one of our recruiters, who will determine whether you qualify for a full or partial Installment Service agreement based on your grades in your school and check your background & skills.

Anytime you want to upgrade your skills and need a helping hand to enter or reenter the tech workforce with high-demand tech skills, reach out to us. Since 2010 we have helped 1000’s of job seekers succeed in the technology sector. SynergisticIT’s career-oriented training programs guarantee fast-paced, quality tech education, preparing you with top-notch skills for coveted tech roles in the industry. Reach out to us. SynergisticIT– Home of the Best Data Scientists and Software Programmers in the Bay Area!